For those few of you who still come back to this blog, I am alive. No activity

for over a year probably had you thinking otherwise. Not much has happened

investment wise over the last year, I didn't find any securities that matched

my selection criteria. Hence the inactivity.

Today, I

am writing about second-level thinking. This is a topic that many of you who

are experienced value investors are already familiar. This is a post that is

probably more useful to the non-investing or the non-value investor

crowd.

Howard

Marks, a renowned distressed debt investor, wrote about second-level thinking

in his book "The Most Important Thing: Uncommon Sense for the Thoughtful Investor". The book is an edited version of his memos (all his memos are here) that he has been

writing to his shareholders for nearly two decades. I highly recommend reading

the book. My favorite chapter is the first one: "Second Level

Thinking".

Marks

contention is that a lot of people do first level thinking, but very few seem

to understand second level thinking. He considers the ability to exercise

second level thinking of utmost importance to achieve market beating returns

over a longer term. What is second level thinking? Let me give you some

examples.

First

level thinking says: "I love this company's products, it has a great

culture. Let's buy the stock." Second level thinking says: "The

company is doing well, but the expectations that its going to do well is

already backed into the price and some more. The company is overrated. Let's

sell."

First

level thinking says: "I think the company's earnings will fall, let's

sell." Second level thinking says: "I think the earnings will fall

less than people expect, so the stock will go up because of the surprise. Let's

buy."

Both of

the above are rather simple examples, thinking at the second level is not too

difficult. So, now that you understand the concept, let me use a real world

discussion I have been having with a colleague (Mr. Page) in my professional

life as an engineer. I consider this colleague to be among the very few smart and

thoughtful people I know of.

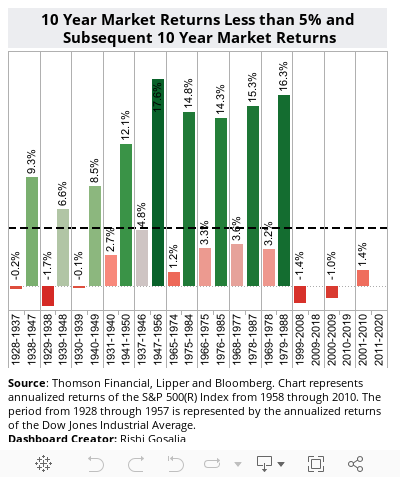

Page:

"You know S&P 500 returns over the most recent decade have been

really poor"

Gosalia:

"Yeah, but historically, all "lost decades" have been followed

by attractive returns for the following decade. Look at the data."

Gosalia:

"This time may be different, but I would not use the most recent decade's

poor performance as the reason for staying away from equities."

Page:

"There are a lot of hidden details behind the numbers you don't see in the

graph that are important to observe. You could look at WWI, New Deal, WWII,

Federal Reserve Act, War on Poverty, Federal Reserve actions (specifically in

1937), Gold Reserve Act, 1971 complete disconnect of the US dollar from Gold,

women entering the workforce, invention of 401(k), real estate easing, general

population getting access to the markets, dot-com bubble, and the real-estate

bubble."

These are

really good observations by Page. But then he makes a first-level thinking

observation, in my opinion: "The government's fiscal situation is

terrible. It's ability to continue to prop up the economy will be limited going

forward. You also have the baby boomers retiring. Baby boomers are the largest

demographic in the country. These retirees, as they pull their money out, will continue

to drag market returns for the next twenty or so years. I don't expect the

economy to go anywhere for the next few decades."

I assuming that his conclusion to the above first-level observation is to avoid equities going forward, but if I am incorrectly interpreting his conclusion. my apologies Mr. Page. Here is my response which I believe is second-level thinking:

"Yes, baby boomers will be

retiring and looking to "pull" out their money. But geez, where will they stuff this money into. Taking all this capital out and putting it into their

"mattresses" is not an option. When capital disappears from one part

of the system it shows up somewhere else. One thing retirees really need

is regular income. Will they pour their massive capital base into fixed

income. That will surely kill any aspirations they have for any regular income.

More money into bonds will bid up bond prices and lower their yields. Combine

it with the fact that yields are already near zero, putting retiree capital

into fixed income is as good as stuffing into their mattress.

I think

its more likely that retiree 401(k) capital will move into high dividend yielding

stocks to support their need for regular income. Hmm, where I am to look for

high dividend stocks. REITS pay out large dividends, don't they? But that's

first level thinking. Everyone knows they pay out all their earnings in

dividends, so the stock prices are currently bid up causing effective

yield rates to be lower. Second level thinking tells me that I should be

looking for companies that have very low dividends currently but have a very

long runway for dividend growth. Wall Street is not expecting them to raise

dividends anytime soon, so their stock price don't account for it.

Hmm, so

what kind of stocks can raise their dividends but haven't done so yet. How

about the banks? Banks don't need much capital to grow, as long as they are

well capitalized, the rest of the capital can be returned to shareholders. The

Fed has explicitly capped dividends for many of the large banks that have

been recipients of bailouts. First level thinking: so you want me to

invest in these "evil-doer" bailed out banks run by irresponsible

managers? Second-level thinking: There are some 7000 banks in the US, and

only a few were responsible for the "evil-doing". In addition, the

Fed "bailed" out many banks that weren't under duress during the

financial crisis to disguise from the general public the banks that were really

under duress.

May be, I

can find a bank run by responsible and trustworthy managers that has a

healthy balance sheet and can grow its dividends. How about Wells Fargo? They didn't use customer

deposits to gamble on derivatives trading. They weren't involved in sub-prime

lending. Their balance sheet prior to the Wachovia acquisition was relatively

clean and easy to understand. Post Wachovia, its already been a few years and

those loans are aging well. They have a lot of capital in reserve to absorb any

future expected losses, more so than going into the financial crisis.

With

strengthened balance sheets, I find it hard to envision such hard dividend caps

on the healthy banks, say 8-10 years from now worst case. Wells Fargo currently

only pays 10-20% of its earnings out as dividend. Management has clearly

indicated that they would like to grow dividend payout ratio to 50%. Combine it

with the fact that housing will eventually come back, causing earnings to grow

as well. If yields rise because of retirees pouring money into fixed income

products, that helps Wells Fargo since it is an "asset-sensitive"

bank - meaning the rate at which it lends goes up higher the rates it has to

pay on its deposits. The deposits they have are very sticky and are unlikely to leave for a higher yield. The spread leads to higher returns on capital.

Second-level

thinking question: Are any of these observations about Wells Fargo baked into

its stock price (at $23 when I purchased the stock in 2011)? Its trading at

book value and less than 10x P/E. Definitely not, Wall Street is simply

ignoring these observations. They don't have a longer time frame like I do. But

may be someone else is making similar observations. Let's check out 13-Ds. Hmm,

Warren Buffett has been buying loads of Wells Fargo stock. Is he thinking along

the same lines?

What kind of returns could I expect buying Wells Fargo at $23 a stock at book value and 9-10x P/E. Well, Wells Fargo has been doing about 1.2% to 1.3% return on assets. It is levered equity to assets by 10x. So, it is currently doing about 12% to 13% ROE. USBank, a close peer to Wells Fargo, has been able to do 1.5% ROA. If Wells can get there in a a year or two, Wells will be compounding book value at 15%. So, book value will be double in about 5-6 years. Current book value is 20-23 (as 2011 when I purchased the stock), so it could easily be at 40-45$ in 5-6 years. But a bank achieving that kind of ROE shouldn't be trading at book but at least 1.5x book value. So, the stock is worth about $65 - $70 given a 5-7 year horizon. Buying at $23, lets just round to $25, you are able to make a 2.5x return on your capital in 5-7 years or 17% compounded return. Another way to look at it is Wells is earning about 3-4$ in EPS. It could be double its EPS in 7 years, so EPS could be at 6-8$. If it pays out 50% in dividends, its paying 3-4$ dividend. Should the dividend yield of the stock be 5%, you get a price of 60-80$. Is any of this pie in the sky - not at all. We have such a huge margin for error buying at $23 that even if things didn't work out as laid out above, the buffer could easily absorb enough wrong things that could happen before I lost money. Much better than stuffing my money in the "mattress" of fixed income or any other alternative asset class (gold, silver, art, wine .. ).

What kind of returns could I expect buying Wells Fargo at $23 a stock at book value and 9-10x P/E. Well, Wells Fargo has been doing about 1.2% to 1.3% return on assets. It is levered equity to assets by 10x. So, it is currently doing about 12% to 13% ROE. USBank, a close peer to Wells Fargo, has been able to do 1.5% ROA. If Wells can get there in a a year or two, Wells will be compounding book value at 15%. So, book value will be double in about 5-6 years. Current book value is 20-23 (as 2011 when I purchased the stock), so it could easily be at 40-45$ in 5-6 years. But a bank achieving that kind of ROE shouldn't be trading at book but at least 1.5x book value. So, the stock is worth about $65 - $70 given a 5-7 year horizon. Buying at $23, lets just round to $25, you are able to make a 2.5x return on your capital in 5-7 years or 17% compounded return. Another way to look at it is Wells is earning about 3-4$ in EPS. It could be double its EPS in 7 years, so EPS could be at 6-8$. If it pays out 50% in dividends, its paying 3-4$ dividend. Should the dividend yield of the stock be 5%, you get a price of 60-80$. Is any of this pie in the sky - not at all. We have such a huge margin for error buying at $23 that even if things didn't work out as laid out above, the buffer could easily absorb enough wrong things that could happen before I lost money. Much better than stuffing my money in the "mattress" of fixed income or any other alternative asset class (gold, silver, art, wine .. ).

So, may

be all of this second-level thinking makes sense on an individual stock level.

But how does that apply to general market returns. What will S&P500 do

over the next few decades. My response: I don't care, my job is not to predict

returns for overall market, but to make investments that produce 12% + inflation

beating returns over the longer term. Questions like what will S&P do

and what will the economy do has nothing to do with investment success at the individual level. Conclusions like "lets avoid equity" because of such and such reason don't really apply."

Howard Marks says that first level thinking is simplistic and superficial, just about everyone can do it. All first level thinking needs is an opinion about the future, as in "the outlook stinks, call for low growth and rising inflation. let's dump our stocks".

Second level thinking is deep, complex and convoluted. The second-level thinker takes a great many things into account:

- What is the range of likely future outcomes?

- Which outcome do I think will occur?

- What does the consensus think?

- How does my expectation differ from the consensus?

- How does the current price for the asset comport with the consensus view of the future, and with mine?

- Is the consensus psychology that's incorporated in the price too bullish or bearish?

- What will happen to the asset's price is the consensus turns out to be right, and what if I'm right?

- ...

I don't claim that I am a second-level thinker and someone else isn't. I know Mr. Page is a very smart man, and he may also be thinking at a second level and I am not aware of those thoughts.

Having said that, the first step is recognize what is needed for investment success. The second step is to start exercising this kind of thinking into our investment process. Currently this is a conscious effort for me to exercise this kind of thinking and not fall prey to first level thinking.

I've been reading your last year's articles on MA/V.

ReplyDeletePutting valuation aside, have you changed your opinion on their moat since?

I think you're reasoning is flawed in that you're assuming an either/or argument?

The banks/merchants don't have to drop MA/V entirely, lose the revenues stream, and adopt the new solution/technology cold turkey. the two solutions can live in parallel for a number of years. And the new entrant could be happy with less than 50% margin, or even breakeven, if they get access to customer data and support THEIR ecosystem (widen their moat).

http://www.google.com/wallet/how-it-works/in-store.html

Now this is still piggybacking MA/V, but once it gets enough traction it could be trouble for the incumbents, I would think.

I agree that I am somewhat wrong about what I originally said. It's not an either/or argument. I agree that Google with its ad supported model is in a great position to disrupt this space. Sequoia Fund folks commented on this topic at their 2012 investor day:

Delete"Mobile payments are a big change for that industry. Right now it seems like a fairly benign change, probably more benign than I would have expected a couple years ago. But as an investor you are well served to approach radical change, even if it looks benign for the moment, with a healthy degree of skepticism and humility. So I reserve judgment on how mobile turns out over the next five years. It's likely to continue pushing along the market share shift away from paper-based payments toward electronic payments, which is certainly a trend that goes in MasterCard's favor. Right now it seems like most mobile payment platforms are going to operate similarly to how PayPal operates today, which is basically as a mobile wallet where you can enter all of your plastic credit card information into the mobile wallet along with your bank account information and basically use PayPal the same way you use your wallet. You can choose which payment card you want to use for any given transaction. You can set one as the default, which most people do in their minds, even if they don't have a computer program in their wallet that does it for them. ..."

"So all that seems pretty benign. One of the big risks of mobile is that in any mobile wallet you are likely to enter your bank account information, which will enable the mobile wallet to pull money directly from your bank account and make an ACH — automatic clearinghouse-based — transfer of that money to whomever you are buying the goods from. That is a form of payment that escapes the MasterCard/Visa universe. There are some merchants online that offer that. If you go to Amazon.com you can give them your bank account information and pay that way. A lot of people, number one, they are reluctant to do that because it's a pain to enter information in every website you go to. Also there's a big trust issue involved; a lot of people don't want to have their bank account information sitting out there all across the Internet. Obviously ACH is something that you cannot do on the ground at a brick & mortar merchant — or you have not been able to do thus far, though that is changing now that PayPal signed up a deal with Home Depot that allows customers to use their PayPal accounts at the point of sale at Home Depot. That is another thing we will have to watch carefully because it brings the ACH modality to the point of sale. But for the moment, at least, your ability to pay that way is pretty constrained. If mobile wallets proliferate and if we see PayPal sign up a lot more offline deals like the one with Home Depot, then your ability to pay by ACH increases, and that is a negative for MasterCard. How all of that shakes out — I think anyone who tells you he knows is just putting you on. ..."

Delete"The other curve ball that you are likely to see is that you have got people involved in mobile now like Apple and Google, who because of the way that universe has emerged, because of the fact that Apple essentially controls a mobile user base in the hundreds of millions of people — Google’s may be over a billion now — may have the ability to start a new mode of payment that really no other participant in the payment's ecosystem has had heretofore. Traditionally one of the best aspects of MasterCard and Visa's businesses is that what they built is just very, very hard to build. There is a huge chicken and egg problem about trying to build out a global payments network. But they did it. They were the first to do it and it took them decades to do it. Other people who have tried going along the same road have largely failed. But Apple and Google, given that the paradigm has shifted, may be able to succeed where others have failed and that certainly would not be a good thing for the associations. So I definitely think about that. You can have very long debates about whether, given the prices that MasterCard and Visa trade for, you are well compensated to take that risk. I think for the moment, you are adequately compensated. But it is something that we watch and we have to pay a lot of attention to."

Deleteinteresting. i had missed sequoia commentary last year.

ReplyDeleteyeah, their moat is still fantastic, but not bulletproof. someone patient and with large pockets can chip away at it.

Hi,

ReplyDeleteI'm also reading this book. I though the book is really classic and we can always find something interesting when re-read the book just as we re-read Graham'books.

It's nice to know your blog today. I will spend time to digest your articles.

Last, I'm from HaNoi, VietNam. It's far far away from TX, US but nice to meet you. ^^

Nice to meet you too Mr. Tung.

Delete